Canadian real estate is entering a new phase — one marked by softer prices, rising HELOC debt, improved affordability, and the first signs of renewed buyer activity heading into 2026. And while today’s headlines paint a mixed economic picture, one thing is clear: the next year will reward borrowers who plan early, understand their numbers, and build flexibility into their mortgage strategy.

As a Brampton Mortgage Broker who works directly with first-time buyers, move-up families, those refinancing, and homeowners navigating renewals, I want to break down what all of this means for you — and what steps can help you get ahead of the market instead of reacting to it.

1. Prices Have Reached a 4-Year Low — But There’s More to the Story

Across the Greater Toronto Area, average selling prices remain below their early-2022 peak. TRREB data show the GTA average reaching about $1.334M in February 2022, while 2025 Market Watch reports have prices generally tracking in the low-$1.1-million range year-to-date — roughly an 18%–20% pullback.

Affordability has improved since the 2022 peak — but borrowers are still stretching far more than they were before the pandemic. Falling bond yields and rising incomes have eased qualification slightly, but the stress test continues to keep many buyers on the sidelines.

Other concerns:

- Buying with a minimum down payment still leaves many first-time buyers with very high loan-to-value ratios.

- A simple price correction could leave some households with little or no equity at renewal.

- Refinancing remains off the table for anyone who cannot reach the 20% equity requirement.

This is where planning, structure, and risk management become just as important as getting a “good rate.”

2. HELOC Balances Are Surging — A Warning Sign to Watch

Canadians are increasingly tapping their home equity again. Bank of Canada data show that home-equity-secured credit (including HELOCs and combined mortgage-HELOC products) has begun rising again after several years of flat or declining balances — even as overall mortgage growth has cooled.

Rising HELOC use isn’t inherently bad — HELOCs can be a smart tool when used strategically — but the trend signals financial pressure.

For Brampton homeowners, this is a moment to reassess your debt, consolidate if needed, and design a mortgage plan that gives you control, not stress.

3. Housing Starts Have Fallen — But Supply Won’t Fix Itself Overnight

Housing starts have fallen across the GTA, particularly for ownership homes. CMHC data and Toronto CMA forecasts point to significantly fewer new single-detached and other ownership units breaking ground than during the 2021 boom period, as higher borrowing costs and softer pre-construction sales continue to weigh on new supply.

For buyers, especially in the GTA:

✔ More choice

✔ Minimal bidding pressure

✔ A buyer’s market heading into the spring of 2026

This is good news — and it creates a more comfortable environment for buyers.

4. Households Are Borrowing More… But Not Through Mortgages

Household credit continues to rise in Canada, but most of the growth is now coming from non-mortgage borrowing. While mortgage balances have levelled off, credit-card, personal-loan, and other consumer credit lines have been growing faster as households absorb higher living costs.

This shift shows households are under strain and using short-term credit to stay afloat. That increases vulnerability — especially if job markets weaken or unexpected expenses hit.

For those renewing in 2026, early planning is more important than ever.

5. Inflation Looks Better on Paper — But Shelter Costs Tell the Real Story

Canada’s inflation rate cooled to 2.2% in October, with most of the improvement driven by sharply lower gasoline prices. When you exclude gas, inflation held steady at 2.6%, showing that underlying price pressures haven’t cooled much. Shelter costs remain one of the biggest contributors to overall inflation, with mortgage interest costs rising 2.9% year over year (Reuters).

6. GDP Looked Great — But the Details Weren’t

Canada’s latest GDP headline looked upbeat, pointing to stronger Q3 momentum — but the underlying details tell a different story. Statistics Canada’s advance estimate shows GDP by industry contracting by about 0.3% in October, signalling softness beneath the surface even before full Q4 data arrive.

With the policy rate now in the low-2% range after several cuts from the 5% peak, conditions are far less restrictive than they were in 2023 — though not strongly stimulative, especially given ongoing trade uncertainty.

7. But There’s Good News: Sales Are Quietly Picking Up

According to TRREB, GTA home sales have stabilized even as new listings ease. GTA home sales rose modestly on a month-over-month basis, marking several increases over the past half-year. New listings edged lower, tightening conditions slightly, while months of inventory held close to balanced levels at around 4 months, depending on home type and region.

With rates in more stimulative territory, demand is quietly rebuilding. If pent-up demand enters the 2026 spring market, competition could heat up.

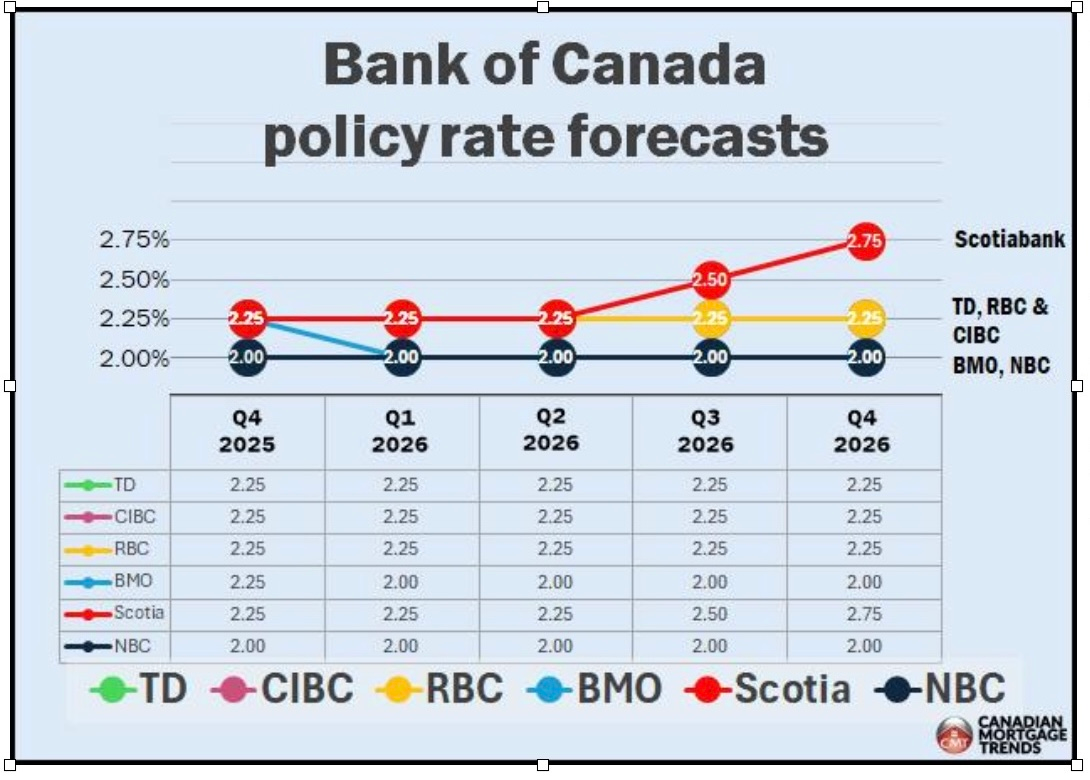

Rate Forecasts Show a Split for 2026

Rate expectations are beginning to diverge across major Canadian forecasters. RBC expects the overnight rate to fall toward 2% and hold there; TD sees a settling point near 2.25%; while Scotiabank projects the rate rising again toward 2.75% by late 2026. This split in forecasts highlights growing uncertainty around inflation, trade tensions, and economic resilience.

Rate expectations are beginning to diverge across major Canadian forecasters. RBC expects the overnight rate to fall toward 2% and hold there; TD sees a settling point near 2.25%; while Scotiabank projects the rate rising again toward 2.75% by late 2026. This split in forecasts highlights growing uncertainty around inflation, trade tensions, and economic resilience.

For Brampton buyers, this split underscores the need to plan for more than one possible rate path — especially when choosing between fixed and variable rates.

8. For First-Time Buyers: 30-Year Amortizations Are Changing the Game

New federal rules are having a real impact:

- Up to 30-year insured amortizations are now available for first-time buyers and for purchasers of newly built homes with insured mortgages.

- Insurable purchase price up to $1.5M, helping buyers achieve homeownership with a lower downpayment and lower insured rates

For many Brampton buyers, this is the difference between qualifying and not qualifying. But stretching to the max requires guidance — especially if the market shifts or prices adjust.

What Brampton Buyers & Homeowners Should Do Now

1. Get pre-approved early

Rates may move, but your approval anchors your strategy.

2. Understand mortgage flexibility

Prepayment rights, penalties, portability — these matter more than ever.

3. Protect your equity

Don’t overextend without a plan for job changes, market dips, or life events.

4. Build a renewal strategy now

2026 will bring a wave of renewals. Don’t wait for your lender’s “loyalty offer.” Get in touch 6-9 months before your mortgage renews.

5. Work with a mortgage broker who understands the Brampton market

Every neighbourhood behaves differently — prices, supply, investor demand, and competition all vary. That’s where Rakhi Madan, Mortgage Broker Brampton, makes a measurable difference.

How Rakhi Helps You Stay Ahead of a Changing Market

As a leading Brampton Mortgage Broker, Rakhi:

✔ Reviews multiple lenders to find the best structure, not just the best rate

✔ Discusses fixed vs. variable based on your real financial goals

✔ Helps first-time buyers prepare documents early and qualify with confidence

✔ Designs renewal and refinance strategies to protect equity and reduce risk

✔ Guides you through new 30-year amortization rules and downpayment options

✔ Helps homeowners consolidate debt through smart, forward-looking planning

In a market this unpredictable, expertise isn’t optional — it’s your safety net.

Final Thought: Today’s Market Isn’t Good or Bad — It’s Transitional

2026 won’t look like 2022, 2020, or 2018. We’re entering a new cycle shaped by:

- softer but stabilizing prices

- rising equity extraction

- renewed buyer activity

- uncertain economic footing led by tariff concerns

Those who prepare early will come out ahead.

Ready to plan your next move?

Whether you’re buying your first home, preparing for renewal, or exploring a refinance, Rakhi will help you build a mortgage plan that fits your goals — not just today’s headlines.

📞 647-886-8710

📍 Rakhi Madan – Your Mortgage Broker Brampton